:quality(80)/business-review.eu/wp-content/uploads/2024/04/Offline-vs.-Online-Wallet-Apps.jpg)

Read more about

:quality(80)/business-review.eu/wp-content/uploads/2020/09/Mihai-Chipirliu-CFA-Risk-Director-Euler-Hermes-Romania.jpg)

The Covid-19 pandemic marked a turning point for ‘unconventional’ monetary policies in Emerging Markets (EMs), several of which embarked on government bond purchase programs to address market dislocations and ease monetary conditions in the short run. However, debt sustainability and inflation are the biggest risks ahead, especially for Brazil, Costa Rica, India, Turkey and Hungary.

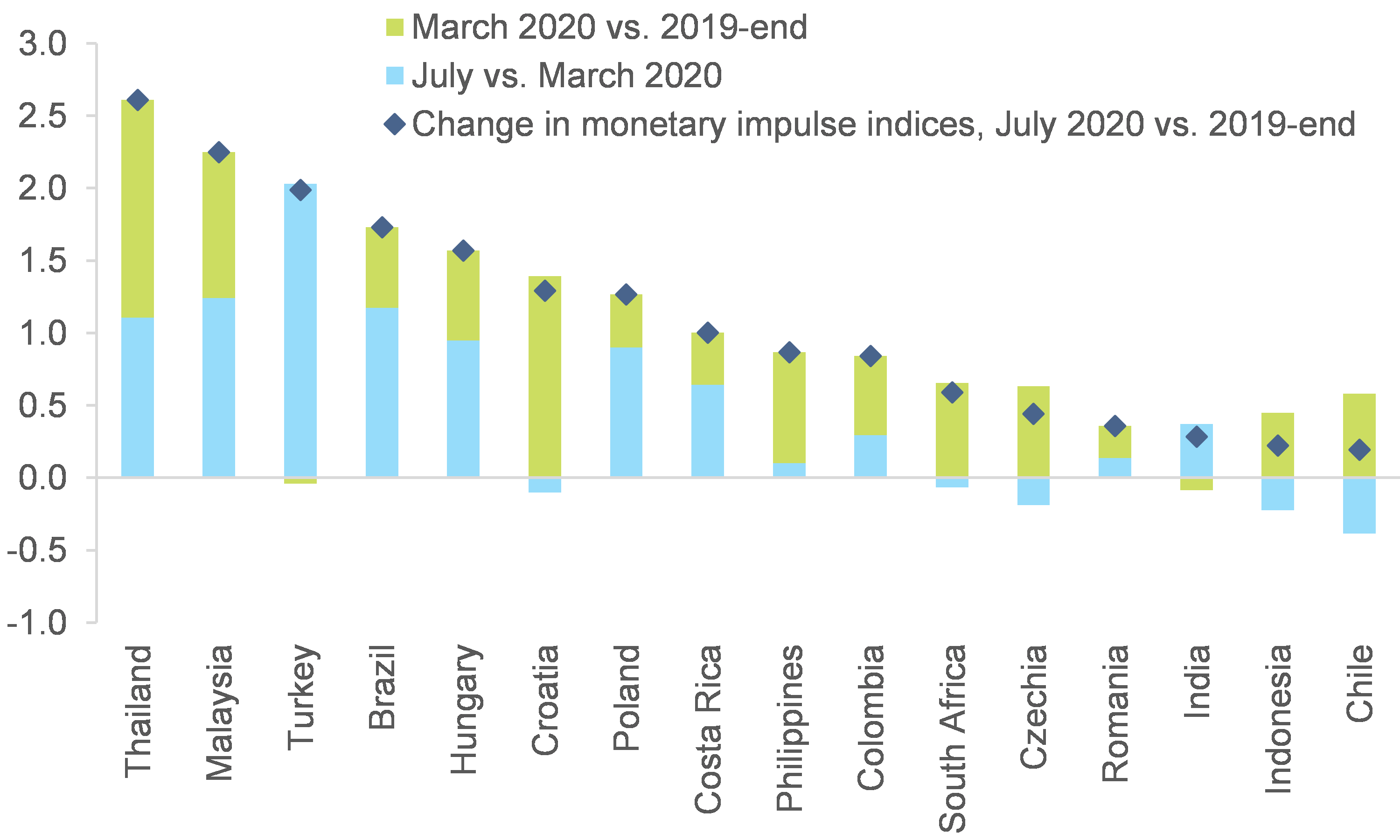

As the pandemic led to investor panic in March 2020, EMs experienced unprecedented net capital outflows (-USD84bn, excluding China), causing dramatic jumps in government bond yields. In this context, 16 EM central banks announced that they were ready to engage in government bond purchases, if needed. Thirteen of them have already started such Quantitative Easing (QE, see Figure 4), instead of cutting policy interest rates that mostly stood well-above the effective lower bound . As a result of these bond-buying programs, long-term government bond yields in our sample of EMs declined by -48bp on average by the end of April compared to the end of March (vs. an average +69bp rise between March-end and 2019-end). The easing of domestic monetary conditions was another short-term success of the QE, as demonstrated by our proprietary monetary impulse indices (see Figure 1). In particular, the indices reached the highest level since at least 2009 (or approached the record) in 12 out of the 16 countries we look at. In the meantime, depreciation of local currencies remained limited (with the exception of a few usual suspects).

The monetary impulse indices are constructed as follows: 1-year change of the 1-year change in M2 money supply (i.e. second derivative), as a share of nominal GDP. They are thus similar to credit impulse indices, but we chose to focus on M2 money supply for ease of comparison across economies. These indices signal how the monetary policy is changing, and tend to lead economic activity.

Notwithstanding the short-term benefits, if pursued intensely, these EM ‘QE’ programmes could cause serious problems in the medium to long run, such as inflation overshooting and debt distress. Systematic bond purchases over a long period of time by a central bank can open the door to debt monetization and jeopardise monetary policy credibility. If QE implies large amounts of liquidity injections by the central bank in local currency, it can become inflationary and also destabilize the exchange rate. In this case, the QE could bring about bigger problems by putting debt sustainability and the private sector’s balance sheets at risk.

The lack of a clear framework on the size and length of ongoing and planned EM ‘QE’ programs could be a concern. While the central banks of the 16 EMs analyzed in this study all stated reasonable objectives (mainly to provide liquidity and ensure a smooth functioning of domestic government bonds markets) for their bond-purchase programs, most of them neither announced a maximum amount that they intend to buy nor a definitive time-frame for their programs. Hence, there is a risk that the QE programs would not be tapered once the objectives have been lastingly reached. For these countries, there could also be a temptation to ease their mounting local-currency debt burdens by simply inflating them. In this context, the QE programs of Indonesia and Poland have generated some concern that the central banks may actually be monetizing state debt beyond appropriate limits. The banks purchased government bonds to the tune of 6.8% and 4.6% of GDP from March to August, respectively, the highest ratios among the 16 EMs. Indonesia’s central bank is to date the only one that has also conducted purchases directly on the primary market, a step normally considered ‘taboo’, though markets have been lenient so far. And regarding Poland, there are worries that if purchases are continued at the current pace until end-2020, the central bank would be financing roughly the entire fiscal deficit of this year, projected at around -8% of GDP.

“As for Romania, although it is in the good half of the top regarding the potential to continue the implementation of quantitative easing, it “catches” the 6th and 5th places in the top of the sustainability risk of debt, respectively of inflation. The factors with the most severe impact in the above classification concern not only the level of public debt but also the high percentage of external public debt in total debt. Also, the relatively low effectiveness of the Government in imposing the necessary fiscal reforms (taking into account the context of the election year and the lack of support in Parliament) and the increase of the M2 composition of the money supply by high correlation with future inflation are other important factors with severe impact. Ultimately, the key issues of vulnerability remain “twin” (trade and budget deficits) deficits. In the absence of spending adjustment measures, the adjustment of imbalances will materialize at the level of the exchange rate – the recent depreciation of the RON is not accidental – and inflation. Last but not least, the effects could be seen in a possible downgrading of the country rating, which would negatively affect the debt financing capacity, the confidence of investors in the economy and the number of insolvencies among companies “, said Mihai Chipirliu , CFA, Risk Director Romania

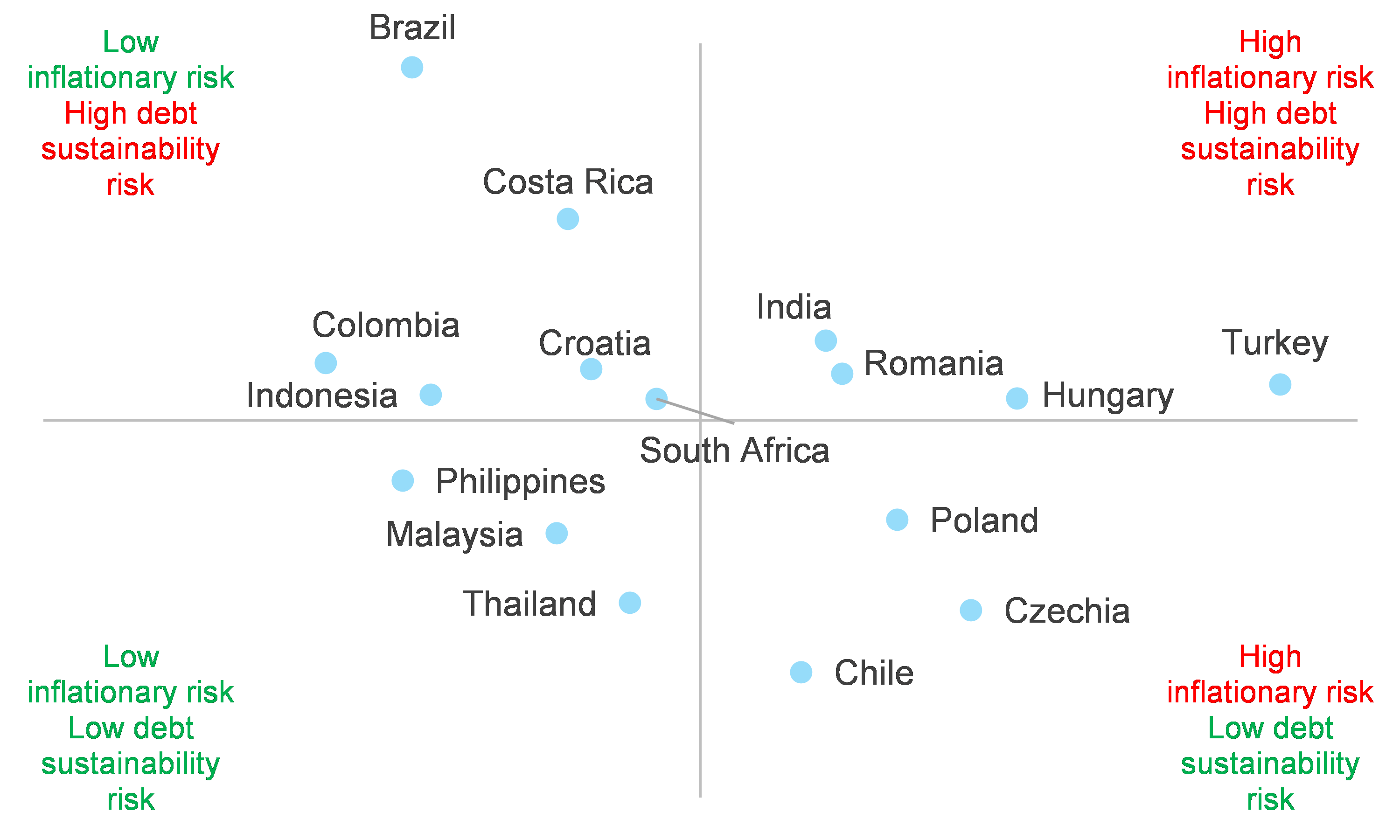

Which EMs pursuing QE face the highest debt sustainability risk? We find that Brazil, Costa Rica, India, Colombia and Croatia carry the highest debt distress risk. Brazil gets the worst ranking in our Debt Sustainability Risk Score owing to its very high public debt and central bank holdings of government debt. At the same time, the low level of government effectiveness suggests the unlikeliness of passing on fiscal reforms to improve the situation (see Figure 5 in the Appendix for details on the score). Costa Rica is ranked second highest risk due to a large interest payment burden and the highest rise in its bond spread YTD (+357bps). However, the bond purchases of Costa Rica, as well as of Colombia and India, have been of modest size so far. Only Croatia’s central bank has already bought government bonds worth 4.2% of GDP since March and thus needs more scrutiny in the near term. Meanwhile, Poland, which has bought more than Croatia, scores well in our analysis, thanks to low interest payments (3.7% of fiscal revenues) and a relatively effective government. Indonesia is not among the top five riskiest markets, thanks to a comparatively low total public debt burden (37% of GDP). South Africa, usually a suspect for debt risks, is ranked average as its high overall public debt (78% of GDP) is balanced by the fast-growing but still low share of FX public debt (11% of the total).

Which EMs pursuing QE face the highest inflationary risk? Turkey, Hungary, Czechia, Poland and Romania show the highest risk of inflation overshooting. Our Inflationary Risk Score signals that Turkey clearly faces the highest inflationary risk as it is the only country with a double-digit inflation rate (11.8% y/y in July) while the current policy rate appears too low (8.25%). Moreover, M2 growth has a high correlation of 79% with future inflation and it rose by +44% y/y in July, the highest pace by far among the 16 EMs we look at (see Figure 5 in the Appendix for details on the score). The four Central European countries that join Turkey in the top five riskiest markets regarding inflationary pressures also have significantly negative real (inflation-adjusted) policy rates while annual inflation has increased in recent months and is now close to the respective central banks’ inflation targets. India, which follows close in rank 6, posted an elevated inflation rate of 6.9% y/y in July and also has a negative real policy rate, but a moderate dependence on the imports of essential goods and a weak link between M2 and price growth.

Debt sustainability and inflation are intertwined as debt monetization increases the public debt burden and raises the risk of inflation. Looking at the combined risks, our analyis identifies Turkey, Hungary, Romania and India as the most risky EMs that have implemented QE-style programs in the wake of the Covid-19 pandemic and crisis (see Figure 2). To close the Pandora’s Box before things get out of control, these QE-like policies should be conducted in a temporary manner and under a well defined framework.

In other words, if the QE-like measures go far beyond accommodative monetary policy, there will be a risk that expansionary fiscal policy will be financed by printing money. This would be nothing new in the EMs history; many EM central banks financed government spending until the turn of the century, mostly with severe consequences such as hyperinflation and sovereign debt defaults.

We derive the Debt Sustainability Risk Score from a set of six indicators across the 16 EMs doing or planning QE: public debt (% of GDP), FX public debt (% of total public debt), government interest payments (% of fiscal revenues), central bank holding of government bonds (% of GDP), the YTD change in the government bond spread, and a government effectiveness index (reflecting the ability to pass structural reforms to increase tax revenues).

We derive the Inflationary Risk Score from a set of four indicators across the selected EMs: CPI inflation rate and real (inflation-adjusted) monetary policy interest rate (as of July 2020), imported inflation risk (share of fuel and food in total household consumption) and the (lagged) correlation between money supply M2 growth and inflation. Importantly, the M2 growth accelerated in all 16 selected EMs in the course of 2020, and it has a positive correlation with consumer price inflation, except for the Philippines and Colombia. For the indicator we chose the correlation with a lag of two months.

Moreover, without a strong fiscal commitment, the short-term relief on local-currency debt markets from the QE-like policies can become counter-productive by discouraging international investors over the medium term.

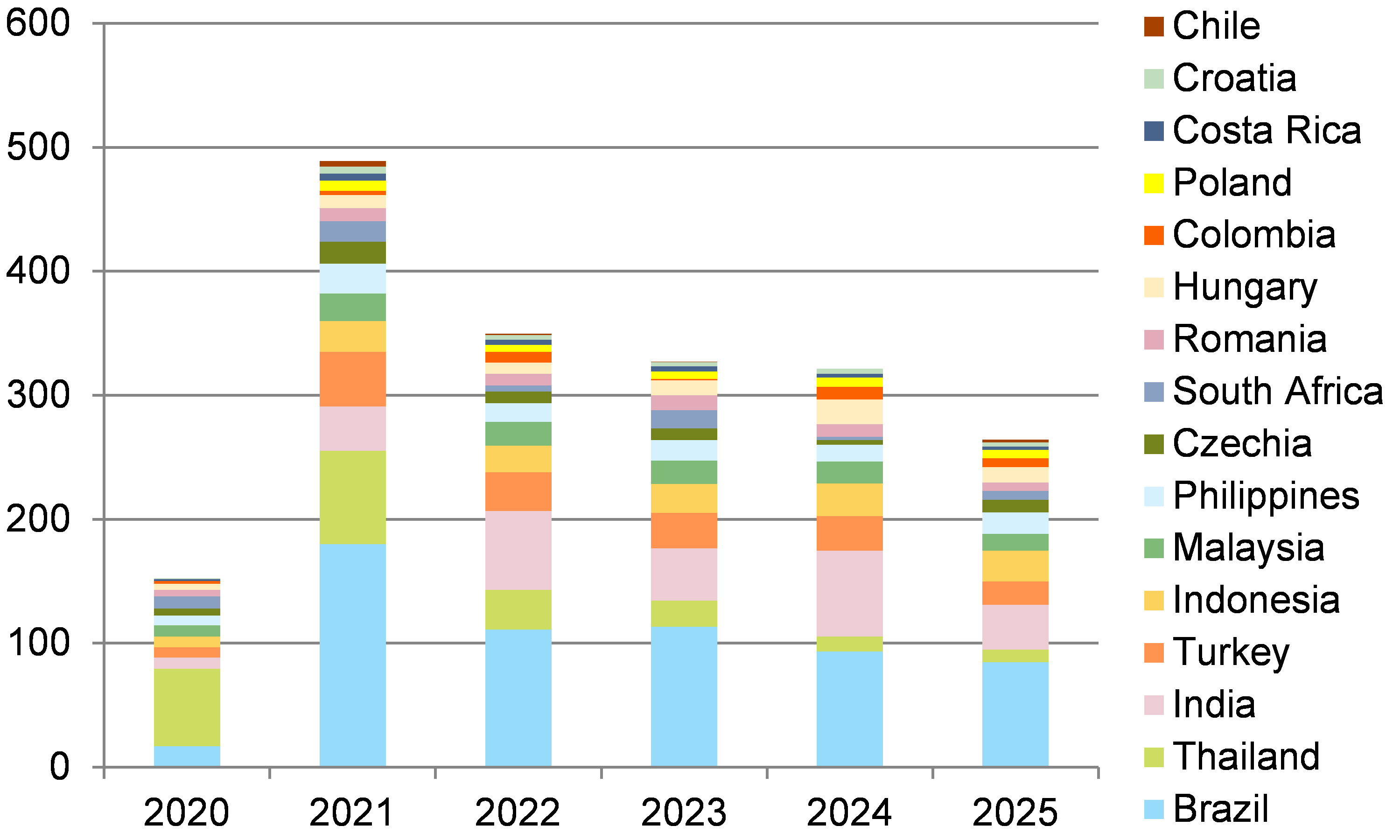

If QE is conducted without a defined time and size framework, it is likely to increase the government’s borrowing cost in the medium term. In fact, amid rising inflation and debt sustainability concerns, investors may ask higher risk premia for new local-currency debt issuances of EMs. This low risk-apetite could be problematic for the EMs that have to refinance maturing debt in the coming years. Figure 3 reveals that the governments of Brazil, Thailand, India, Turkey, Indonesia and Malaysia each have to roll over more than USD50bn of public debt by the end of 2022. In addition, Fed is expected to normalize its monetary policy as of 2022. This may add extra pressure to the borrowing cost of the EMs that conduct large amount of QE without showing credible fiscal consolidation efforts.

:quality(30)/business-review.eu/wp-content/themes/business-review/assets/images/no-picture.png)

:quality(80)/business-review.eu/wp-content/uploads/2024/04/COVER-1.jpg)

:quality(80)/business-review.eu/wp-content/uploads/2024/04/cover-april.jpg)