:quality(80)/business-review.eu/wp-content/uploads/2024/07/vodafone-RO.jpg)

:quality(80)/business-review.eu/wp-content/uploads/2020/11/conf_tmrw.jpg)

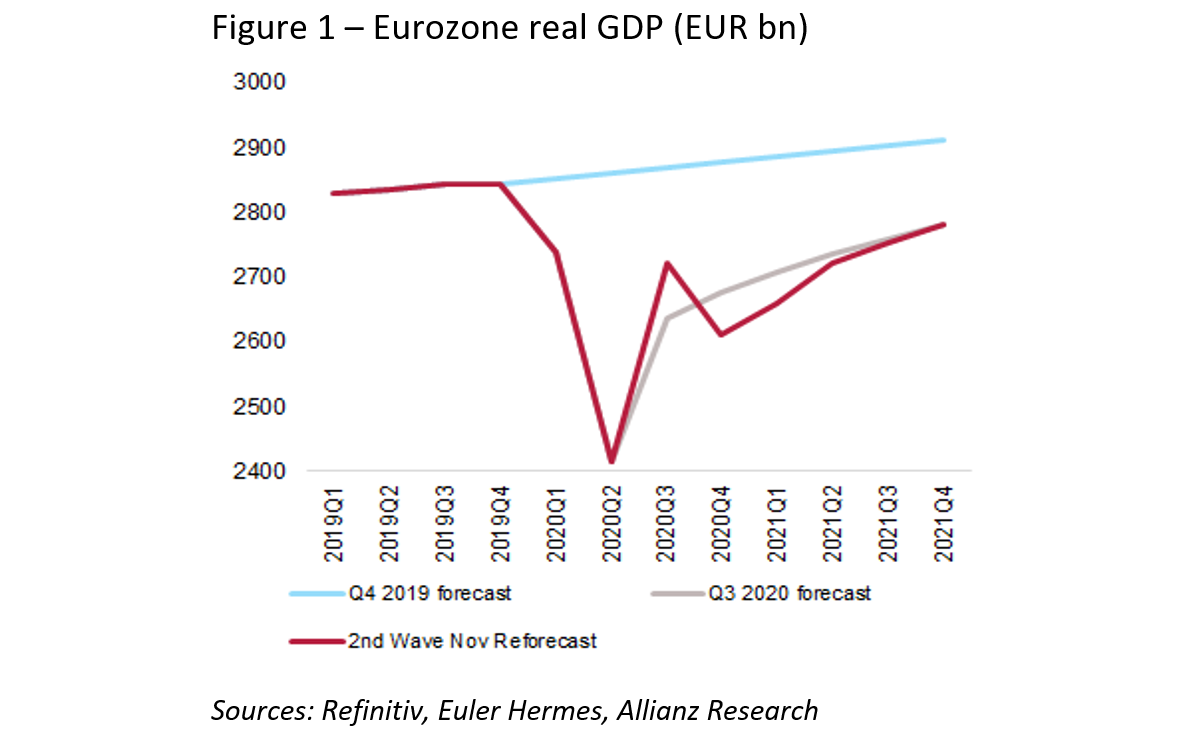

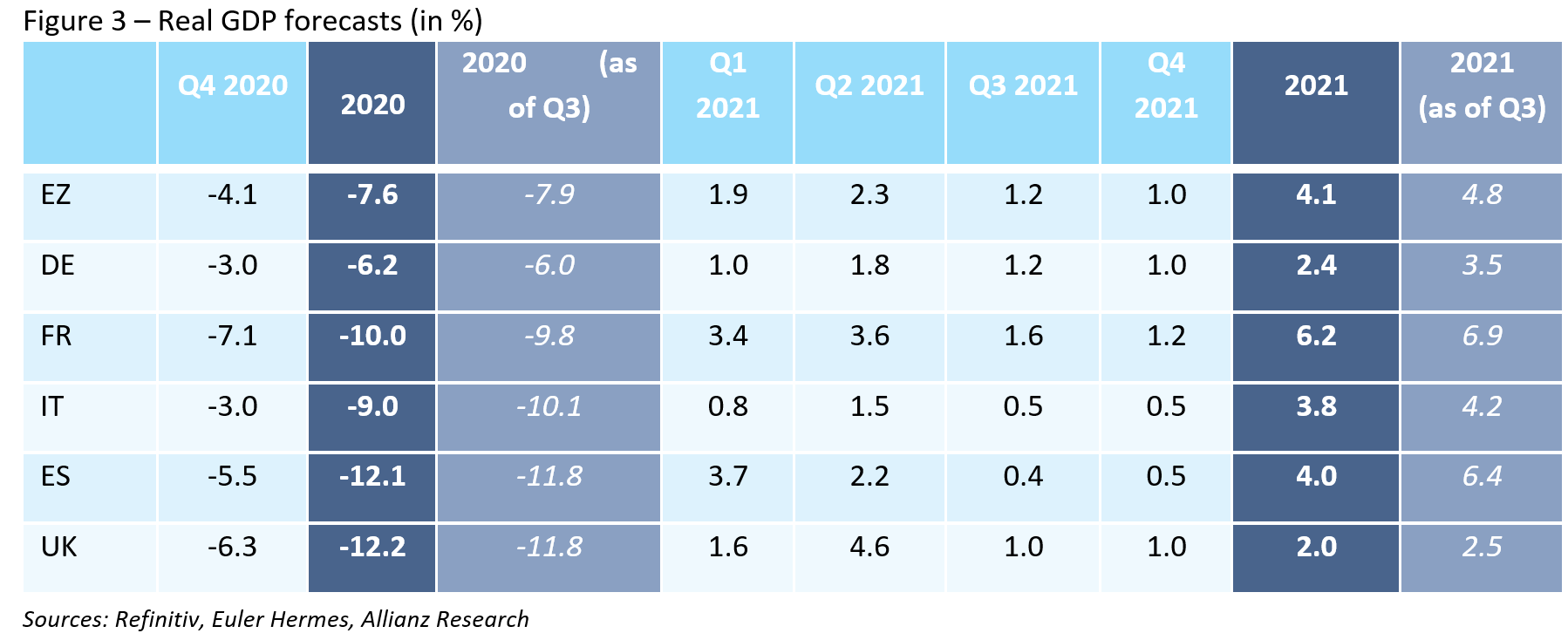

Lockdown 2.0 or ‘lockdown light’ in Europe embodies the stop-and-go strategy, which should follow epidemic cycles until a post-vaccine return to normal in 2022. Yet these new restrictions are not a replay of Spring 2020 as their economic hit to Q4 2020 GDP should prove 30-60% less severe. The Eurozone recovery could thus be delayed but not derailed. Q4 2020 GDP looks set to contract by around –4% q/q, bringing the full-year 2020 forecast to –7.6%. However, expect a timid recovery in 2021 (+4.1% vs +4.8% expected at end September) as strict rules on social interactions remain in place.

Only in the second half of 2021 will the anticipated availability of an effective vaccine, to be rolled out before year-end, provide some much needed tailwind to the economic recovery by reducing economic uncertainty. Nevertheless, the risk of long-term scarring to the economy has risen in the face of more insolvencies, higher unemployment and increased pressure on the banking sector.

A long (European) economic winter is coming

A Eurozone Q4 double dip is all but certain, given the second wave of lockdowns. The stronger-than-expected growth rebound in Q3 with GDP growing by a record-setting +12.7% q/q proved that Eurozone economies can rebound rather swiftly as restrictions are lifted. The big question now is if they can do that again. After all, the fresh round of tough restrictions announced in recent weeks is all but certain to plunge the Eurozone economy back into a contraction in the final quarter of this year.

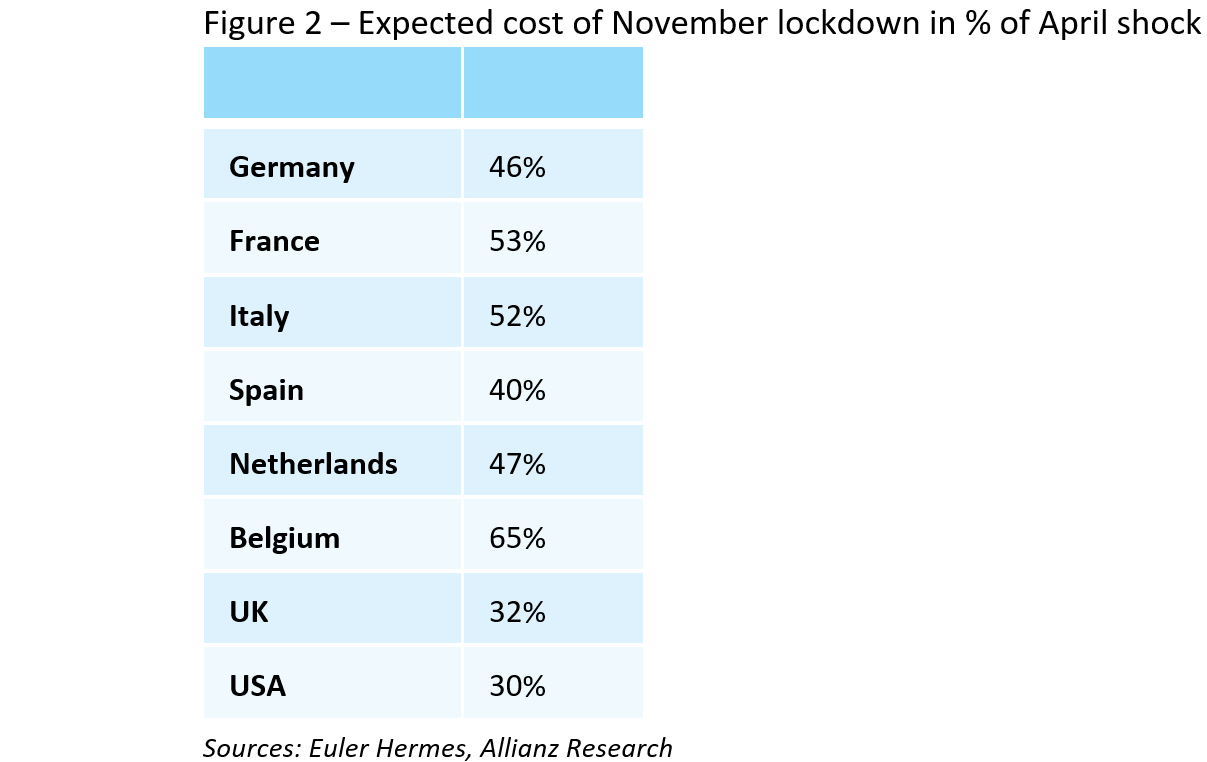

However don’t expect to see an H1 2020 replay: there are important differences compared to Europe’s first lockdowns. The good news first: the impact on short-term economic activity is likely to prove less severe. We expect the lockdown in November to inflict 30-60% of the economic pain on Eurozone economies compared to the April shock as i) measures are more targeted, mainly impacting social spending (30-45% of private consumption) and less restrictive (schools and non-essential businesses are kept open in most countries), which should prop up manufacturing and construction activity and in turn reduce the April shock by 5pp; ii) businesses have gained experience in navigating tough lockdown restrictions (mainly by working more with digital solutions); iii) the most impacted sectors have not yet returned to pre-crisis levels of activity, suggesting fresh lockdowns will trigger a less steep drop and iv) external trade of goods is expected to prove more supportive than in Spring, with China playing the role of a stability anchor. Overall, we see Eurozone GDP contracting by around –4% q/q in Q4 2020, bringing the full-year 2020 forecast to –7.6%. However, downside risks to our forecast, particularly related to the development of the health situation and the resulting negative impact on private-sector confidence, loom large.

The reinforced divergence between on the one hand hard-hit services where value-added still registered around 20% below pre-crisis levels in Q3 despite the strong rebound and relatively resilient manufacturing and construction on the other hand which are only down around 5% could see governments save up to 5pp of GDP growth for a month of lockdown.

However, the bad news is that the recovery momentum following the second reopening is likely to prove more subdued, even when accounting for a smaller growth shock. For one, governments are less likely to ease restrictions to the degree seen over the summer months in an effort to learn from the mistakes that led to lockdown 2.0. In particular, we expect strict rules on social interactions to remain in place to reduce the risk of a sanitary relapse and in turn a triple-dip recession, while countries need more time to set up adequate track, trace and isolate systems. Meanwhile, some economic activities may not see a restart at all until a vaccine and/or more rapid testing is available (for instance larger gatherings and events but also travel activity). As a result, Q1 GDP growth looks set to underwhelm at +1.9% q/q.

An economic resurrection just in time for Easter

We expect European deconfinement to enter a new chapter only in Q2 2021 as adequate health sector capabilities will allow for a further lifting of restrictions. At the same time, warmer temperatures around Easter could keep a lid on the growth rate of Covid-19 cases and provide a tailwind to outdoor social spending. However, elevated levels of economic uncertainty amid lingering concerns about a possible third lockdown and in turn a triple-dip recession will continue to weigh on the rebound momentum as firms and households hold on to excess precautionary savings. Only in the second half of 2021 will the anticipated availability of an effective vaccine, to be rolled out before year-end, provide some much needed tailwind to the economic recovery by reducing the heightened level of economic uncertainty. However, as the vaccination campaign may take several months to be completed, the impact of the seasonal weather change on the spread of the virus may call for a limited step-up in restrictions starting in September 2021.

Overall, we expect the second wave of lockdowns to delay but not to derail the recovery in 2021, with Eurozone GDP set to stage a more moderate recovery of +4.1% vs. the +4.8% expected as of end-September 2020. Hence, a full return to business as usual is not on the cards before 2022, while for the Eurozone as a whole, pre-crisis GDP levels will only be reached at the turn of 2022/23. Even then, the risk of long-term scarring to the economy has risen in the face of more insolvencies, higher unemployment and increased pressure on the banking sector.

Desperately seeking an adequate policy response

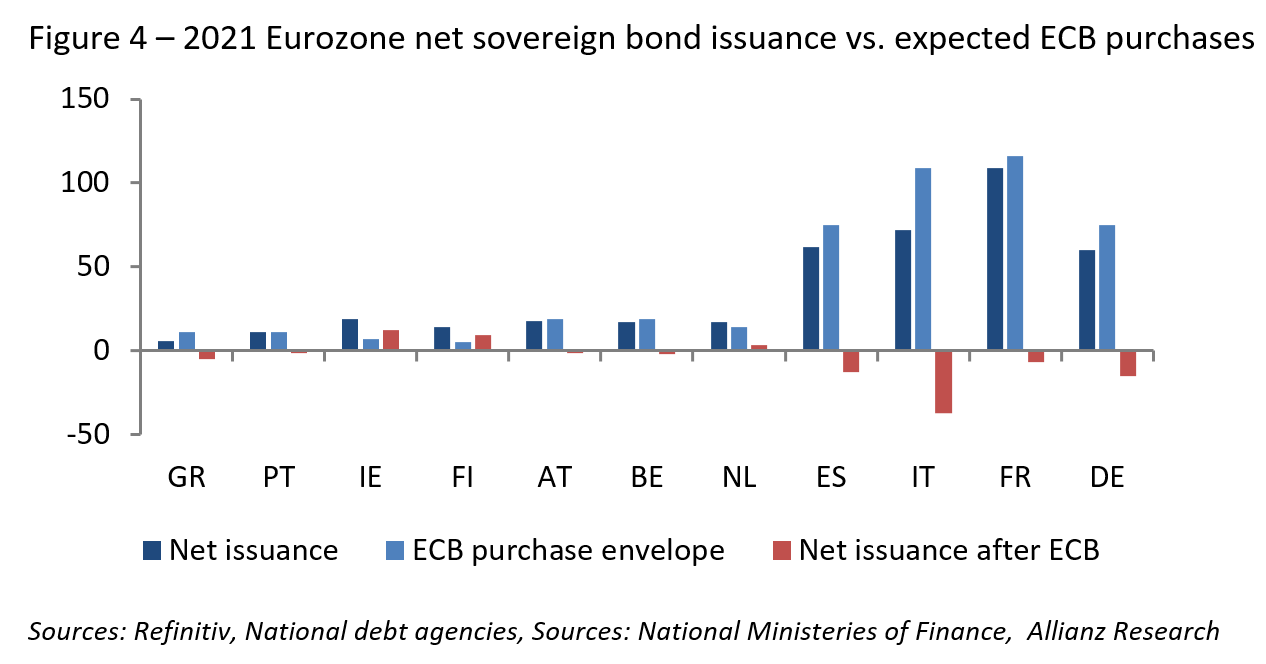

For our baseline scenario to hold, policymakers will have to swiftly upgrade their crisis policy response, with a view towards propping up private sector confidence, averting a “triple-dip” recession and keeping a lid on permanent damage to the economy. In this context, health comes first. Without an adequate ability to track, trace and isolate Covid-19 cases, the second wave of lockdowns will also go to waste. Meanwhile, on the fiscal front, at a minimum measures aimed at limiting long-term damage to the economy – i.e. short-work schemes and public credit guarantees – need to be swiftly extended for as long as restrictions on economic activity remain in place. While national governments are clearly in the driving seat here, EU initiatives that act as second lines of defense by extending national safety nets – above all the SURE program as well as the EIB’s pan-European guarantee fund for corporate loans – are gaining importance and should be topped up on a needs basis. Moreover, hurdles around the implementation of the EU recovery fund needs to be addressed urgently to avoid a delayed or reduced impact. Last but certainly not least, the ECB will need to continue to flank the fiscal expansion of Eurozone governments by recalibrating its policy strategy at the upcoming December meeting. We expect to see a EUR500bn boost to its QE program for 2021 to keep a lid on refinancing costs for governments as well as the private sector. The additional fire-power should be more than enough to absorb the entire expected net issuance of sovereigns, which we estimate to come in at EUR400bn. In addition, the ECB is likely to make terms on TLTRO-III more favorable and could also increase the tiering multiple to provide more breathing space to banks.

What does this mean for corporates?

A large-scale corporate cash-flow crisis will be avoided, thanks to fiscal relief measures and continued liquidity support, but the double-dip recession should further weaken corporate confidence. The share of SMEs which have a negative EBITDA margin, i.e. those most at risk of a cash-flow crisis, is estimated at between 15-20% in the four biggest Eurozone economies, and the share of zombie SMEs – those with high debt levels, low profitability and low equity ratios – stands between 8-10%. In Q2, during the first lockdown, French corporates seem to have lost the most in terms of profitability (-4.0pp to 25.5%) despite an unprecedented strong fiscal support. In Germany, profitability remained broadly stable (+0.2pp to 36.6%). French corporates also registered a strong fall in cash from operating activities: -EUR45.5bn against -EUR19.5bn in Germany, even though tax deferrals and the partial unemployment program explain the higher size of state-guaranteed loans in France (more than EUR120bn against EUR50bn in Germany). However, with the double dip, confidence effects could prove more dangerous by discouraging companies to cover the cash-flow issue with additional debt in an environment where turnover growth in the hardest hit sectors is not expected to go back to pre-crisis levels before 2023.

What does this mean for capital markets?

Firstly, one could expect a modest steepening in sovereign yield curves, more so in the U.S. than in the EMU in line with the rapid increase in public deficit and debt ratios. In a politically conflictual context, markets may get concerned about debt sustainability. While being ready to expand Quantitative Easing further, central banks will want to indirectly subsidize commercial banks, which are currently rapidly expanding their holdings of government bonds.

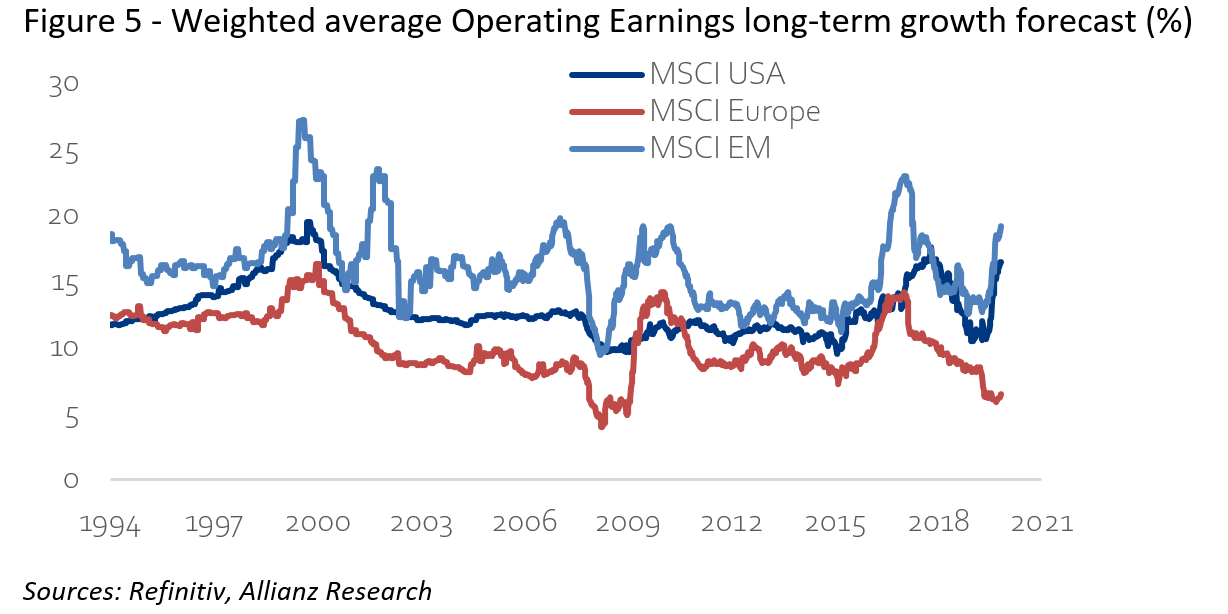

Secondly, on the equity side, overvaluations are more worrisome in the U.S. and EMs than in Europe as they provide little cushion against adverse outcomes. According to IBES, the growth forecasts for long-term operating earnings in the U.S. and EMs currently stand at +16% and +19%, respectively. The same can be said of the shorter-term S&P 500 EPS growth forecast, which is +24.5% for 2021 and +16.8% for 2022. Long-term expectations are more reasonable in Europe (+6.2%), but short-term expectations exhibit the same optimistic pattern as in the U.S.: +39% in 2021 and +17% in 2022. Yes, European equities are not as overpriced as U.S. ones, but correlations between these asset classes jump to high levels when U.S. equities struggle. The overvaluation of U.S. equities is a sword of Damocles over European equities and also a downside risk to the USD: having taken part in the U.S. equity rally, it will take part in its correction.

Thirdly, our worries regarding the corporate bonds segments have increased, notably for the high-yield segment, as lending to insolvent businesses is not part of central banks’ classic job description. Corporate bonds have attracted a lot of fresh capital since March in the wake of central banks’ policy announcements in favor of investment grade bonds (and fallen angels in the U.S., with the ECB possibly jumping on the bandwagon as soon as December). However, especially in the EMU, it would be a mistake to assume that the central bank can backstop any kind of corporate bonds regardless of their creditworthiness. National Treasuries will have to do that job, hopefully but not necessarily in a timely manner. Spreads at the lower end of the credit spectrum will therefore widen. In EMs, even if the long-term growth outlook is more attractive than in DMs, an operating earnings long-term growth forecast of +19% provides little cushion against adverse outcomes. Owing to past currency depreciation, local currency bonds offer some value, but at the cost of elevated volatility. Despite some recent correction, hard currency bonds still look overpriced.

CEE: The cost of new lockdowns

The EU member states in Central and Eastern Europe (CEE) experienced a very mild first wave of Covid-19 infections in spring 2020, thanks to early and stringent confinement measures. However, following a significant relaxation of the lockdowns during the summer, most countries in the region are now experiencing a very strong second wave of infections. As a result, new lockdowns have been implemented, at varying stringencies: Czechia, which is experiencing one of the strongest second wave of infections in all of Europe, as well as Poland have so far imposed the most stringent measures, while Hungary, Slovakia and Bulgaria apply so-called partial or light lockdowns; Romania applies a more regional approach. However, the latter four countries are likely to reinforce their measures should the numbers of new Covid-19 cases continue to rise.

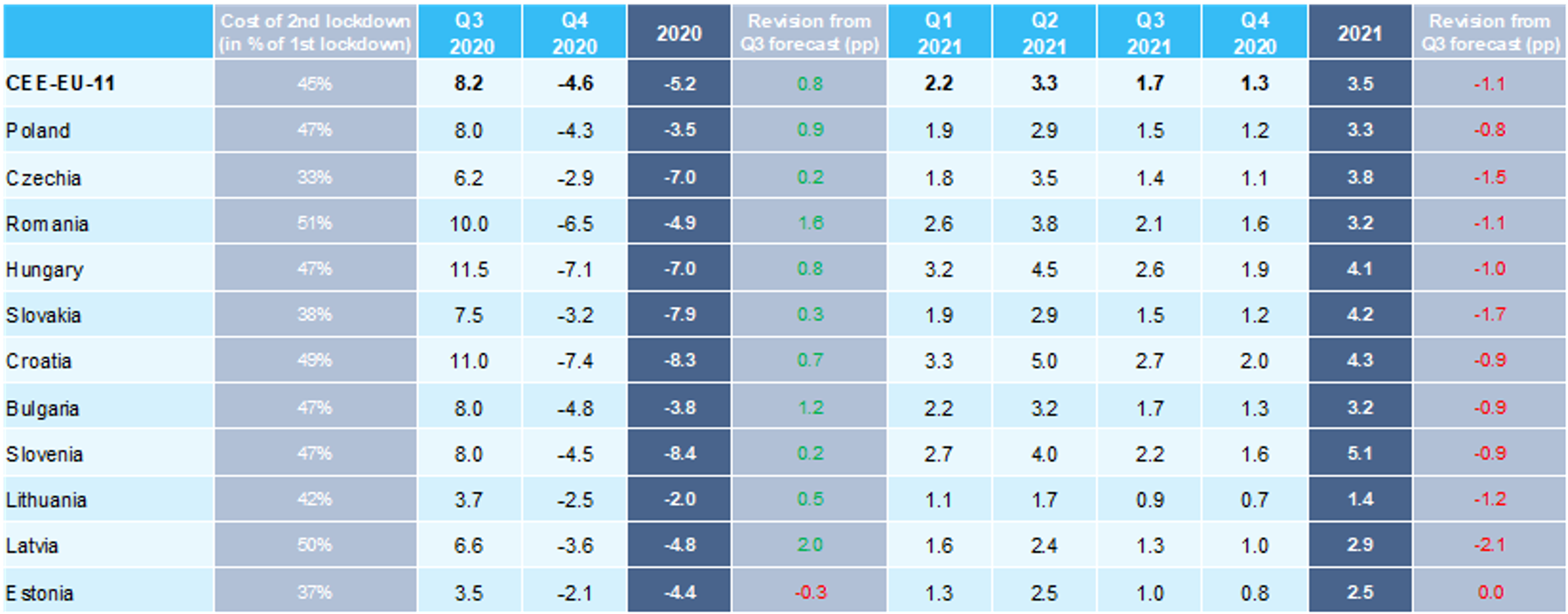

As a result of the latest developments, we have revised our GDP growth forecasts for the region. The overall economic cost of the second lockdowns is expected to be smaller than during spring. The main reason is that the measures are more targeted and thus mostly affect only “Covid-19-vulnerable” services sectors (for example trade, transportation, hotels and restaurants, education, social work, leisure and sports activities), while industrial sectors, construction and agriculture will hardly be affected this time. The economic cost of the second lockdowns is also varying across countries, depending on the size of the affected services sectors, the stringency of the lockdowns, the export dependence, the sanitary situation, the (remaining) fiscal policy leeway of the governments and the overall confidence in the poicy responses. Overall, we now expect double-dip recessions in the region (after Q2 2020, renewed quarterly GDP contractions in Q4), more moderate rebounds in Q1 2021 than in Q3 2020, followed by a strengthening in Q2 2021. In H2 2021, growth should moderate again somewhat as confinement measures should be kept more stringent than a year earlier in order to avoid a third wave of infections and lockdowns. The table below shows our new quarterly and full-year growth forecasts for CEE. Annual growth for 2020 for the whole region was revised to -5.2% from -6.0% in September – the upwards revision is due to significantly better than expected growth in Q3 which does more than offset the expected contraction in Q4. The latter, however, implies a strong negative base effect for 2021, so that growth for all of next year was revised down by -1.1 basis points to +3.5%

Country focus: The costs of “lockdown light” in Germany, France, Italy, Spain and the UK

For Germany Chinese demand as a “pillar of stability” will prove ever more important in the coming months as key trading partners are tightening Covid-19 restrictions to battle the second virus wave. In Germany, GDP jumped by +8.2% q/q in Q3, with the annual rate recovering from -11.3% to -4.3%. Following the announcement of a four-week lockdown in November to save Christmas, we now expect a contraction of -3% q/q for Q4 2020 (-7% m/m in November – around 50% of the April shock), followed by a relatively muted rebound of +1% in Q1 2021 as social distancing restrictions are likely to remain elevated until Easter 2021. The renewed lockdown will delay but not derail the German economic recovery also thanks to the announcement of additional fiscal support to the tune of EUR10bn and the expected extension of flagship fiscal policies, including public credit schemes until at least mid-2021. A tailwind from China is one additional factor that has contributed to Germany emerging faster and in a better position from the Covid-19 shock relative to its European peers. After all, about half of EU-27 exports to China are from Germany. As German export prospects are bound to take a hit with a Eurozone Q4 growth double-dip all but certain, relatively more resilient Chinese export demand provides a ray of light amid the doom and gloom. In fact, out of Germany’s top 10 trading partners, China stands out as the only country that we expect to avoid a pronounced tightening in Covid-19 restrictions. All in all, German GDP looks set to contract by -6.2% in 2020 vs. -6% expected previously, followed by a more muted recovery in 2021 of +2.4% vs. +3.5% previously. As a consequence, we expect the German economy to recover to pre-crisis GDP levels only in late 2022.

In France, the stronger-than-expected economic recovery in Q3 (+18.2% q/q) ought to be short-lived as the economy will slide into a strong double-dip recession in Q4. French GDP rebounded by +18.2% in Q3, driven by strong base effects post lockdown but also by robust consumer spending during the summer. However, with increasing infection rates, both consumer spending and confidence deteriorated in September. The failure of partial containment measures to curb the explosive spread of the virus resulted in a return to a national lockdown as of November. France is implementing a lighter version of the March-April lockdown, with one third of the economy being put on pause for at least four weeks. We expect a less severe loss of economic activity (-16% compared to pre-crisis levels) this time around compared to the previous lockdown (-30%). However, in view of the saturated hospital capacity in most cities, we expect the national lockdown to be extended in December (for at least two more weeks) and be lifted only partially (with curfews in place) during the end-year holiday season. Overall, we expect GDP to plummet by -7.1% q/q in Q4 2020, bringing the annual contraction in 2020 to -10% (from -9.8% expected previously). The second wave of the pandemic will take its toll on the economy, causing severe output losses in already weakened sectors (tourism, hospitability, recreation, and transport and retail trade). Significant fiscal relief measures have been reinstated. In November, the French government announced an additional EUR20bn (1% of GDP) support package by reloading the partial unemployment scheme and the Solidarity Fund. This constitutes the 4th amendment to the 2020 finance law, and will bring the fiscal deficit to -11.3% of GDP in 2020 (up from -10.2%). In 2021, we expect stringent sanitary measures to remain in place in January and February, before being progressively relaxed as of March. Thus, we project a moderate rebound of activity (+3.4% q/q) in Q1 2021. Domestic demand is expected to bounce back with the progressive re-opening of the economy in Q2 2021 (+3.6% q/q). Under the impulse of the EUR100bn stimulus package and positive confidence effects following the start of the vaccination campaign we expect a robust recovery in H2 2021.

In Italy, the lack of a strong fiscal policy tailwind is likely to weigh on its growth performance at the turn of 2020/21. Preliminary Q3 GDP data for Italy shows a strong rebound of +16.1% q/q in Q3, driven by private consumption as well as strong external demand. This is reflected in robust industrial production, which, thanks to the economy’s position in the global value chain, is now close to pre-crisis levels. However, infections have increased since mid-October. While the dynamic remains weaker than in France or Spain, some restrictive measures have been restored, targeted at bars and restaurants (reduced opening hours), as well as leisure and cultural activities (entirely closed). But there are major differences among regions, with measures in the Northern economic strongholds being closer to the soft lockdown in Germany. That means that the Italian retail and industrial sector remains fully working. Nevertheless, a Q4 GDP contraction is all but certain. In addition to the effect of the confinement measures, industrial momentum is likely to weaken due to inventory reductions. We expect economic activity to drop by -3.0% q/q in Q4 and the recovery is likely to remain muted in early 2021 since we see the risk of a fiscal stimulus gap despite more announcements on the fiscal front (the Italian government has approved an additional package of compensatory measures worth EUR5.4bn combining grants, tax deferrals/cancellations and the extension of the short-term work scheme until January 2021). In particular, several support measures for households and businesses could come to an end at the turn of the year. Moreover the measures from the national recovery plan (EUR150bn according to the draft by the Ministry for Economic Development) are mainly supply-side-oriented and have longer lead times, which will hardly allow for a quick implementation. All this means that we have revised our GDP growth forecasts. Even with a setback of -3.0% q/q in Q4 we now expect real GDP to contract by –9.0% in 2020 (-10.1% previously). At the same time, with the adverse carry-over of Q4, we need to adjust our GDP growth forecast for 2021 to +3.8% (previously +4.1%).

Spain lags its European peers in sanitary and fiscal response. Q3 GDP growth was also stronger than expected, but activity was still -9.1% below pre-crisis levels. This time around, new lockdowns or confinamiento should also be “light” for the Spanish economy (closing of non-essential services but continuation of construction, manufacturing and education) and hence less damaging: we estimate the monthly shock could be 40% of that of April i.e. activity would run at close to 86% of October levels. Therefore, with a one-week lockdown in the country’s economic centers, GDP could contract by around -2% q/q in Q4. However, it is likely that the government will also announce a month-long national lockdown in the next days or weeks, given that new cases have kept hitting new record highs in the past week. This leads us to revise our previous GDP forecast for Q4 from -1.3% q/q to -5.5% q/q. December would see a recovery but in Q1 restrictions would remain tighter than after the first confinamiento, leading to a meagre +1% q/q growth then. Spain’s laggard status in the Eurozone should be confirmed: After a contraction of –12.1% in 2020 we expect a a recovery of only +4% in 2021 due to high unemployment, still very subdued tourism activity and uncertainty around the EUR72bn stimulus adoption and implementation. Real economic activity would remain -8% below pre-crisis levels at the end of 2021.

In the UK, Brexit is likely to act as a drag on the post-lockdown recovery. The cost of the second lockdown is expected to go up to one third of the previous one. Social spending, primarily impacted by the lockdown measures, accounts for 48% of GDP. Hence, by accounting for two thirds of the previous lockdown impact from April, and a limited recovery in the rest of the economy, we forecast GDP growth to fall by around -9% m/m in November and to recover only slightly in December (+2% m/m) if a limited reopening is possible around Christmas. Overall, we expect Q4 GDP to fall between –5% and –6% q/q. Fiscal relief measures similar to the ones from March have been reactivated (partial unemployment scheme, tax and mortgage repayments deferrals, public guaranteed schemes), which should add around 1.5-2pp of GDP to public debt. However, the fiscal relief measures coupled with additional QE purchases to the tune of GBP100bn by year-end (the equivalent of 5% of GDP) will play a significant stabilizer role and keep solvency risks in check. Our baseline scenario (a last-minute deal with the EU) has considerably gained traction during the past two weeks, notably as the sanitary situation has worsened across Europe. On the back of the generalized (lighter) lockdowns in Europe, a (short) technical extension of the transition period is likely to avoid disruption at the border due to the custom checks implementation on the date of the EU exit. Hence, Brexit is expected to cut -2.5pp from the recovery post lockdown in Q2 (to 4.5% q/q). Overall, we expect GDP growth to reach +2-2.5% in 2021 as the cost of Brexit would not be fully compensated for by the expected fiscal stimulus (around 3% to 4% of GDP, mainly focused on infrastructure spending and lowering consumer taxes to reduce the burden of higher import prices post Brexit).

What can we learn from other countries’ management of second waves of Covid-19?

Several economies in Asia-Pacific have already been through and brought under control second waves of Covid-19 infections. In Vietnam, Australia and Hong Kong, more stringent containment measures were implemented swiftly after they broke out (in June-July). The peaks of the outbreaks were reached between one and two months after their starts, and a very gradual easing of containment measures started only around one month later. In particular in Australia, a targeted long lockdown of nearly four months was put in place in the state of Victoria, the epicenter of the second outbreak. Easing of restrictions only began when the number of daily new infections dropped to nearly 0. In South Korea, the stringency of containment measures didn’t change much across the second wave of infections and the containment strategy mostly relied on rigorous contact tracing and isolation. On top of more stringent sanitary measures, policy measures to support the economy were topped up. In Australia for example, the wage subsidies scheme was extended by six months when the second wave of infections broke out (increasing the size of the program from 3.3% to 6.2% of GDP). According to our analysis, the confinement measures currently being implemented in Europe are coming at a later time compared to the experience in Asia-Pacific. The peaks of the current outbreaks in Europe could thus be higher and later than in Asia-Pacific.

:quality(30)/business-review.eu/wp-content/themes/business-review/assets/images/no-picture.png)

:quality(80)/business-review.eu/wp-content/uploads/2024/06/COVER-1-4.jpg)

:quality(80)/business-review.eu/wp-content/uploads/2024/06/br-june-2.jpg)