:quality(80)/business-review.eu/wp-content/uploads/2024/07/vodafone-RO.jpg)

:quality(80)/business-review.eu/wp-content/uploads/2018/03/international-trade.jpg)

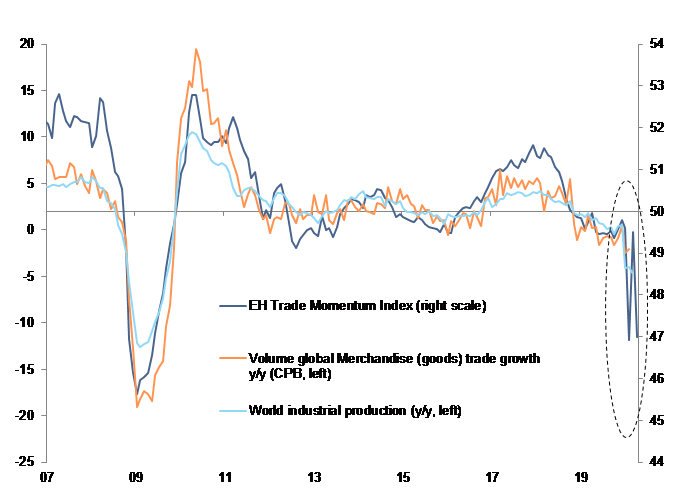

Q1’s strongest contraction in merchandise trade since Q1 2009 is only the first part of the story. Euler Hermes’ proprietary Trade Momentum Index shows that Q2 is likely to see an even stronger contraction (see Figure 1). Indeed, April could post a -13% y/y drop.

Overall trade contracted -2.5% q/q in Q1 as March posted a third straight negative figure (-1.4% m/m and -4.3% y/y). In March, China’s exports rebounded by +12.4% m/m (+2.3% y/y) as the economy restarted, while the Euro area suffered the largest blow, -7.7% m/m (-10% y/y), as its largest economies were on pause. We expect the trough to be reached in Q2, with half of global GDP under lockdown in April and Chinese exports stuttering in search of missing demand, as shown by even weaker export orders.

World merchandise trade prices in USD contracted even more in March (-3.6% m/m), bringing the Q1 figure to -6.2%. This is the result of the oil price shock and the overall commodity price drop as China and then Europe’s demand came to a halt while the dollar significantly appreciated. For exporters, the price effect should aggravate the demand shock, weighing on export revenues.

Yet this picture overlooks trade in services, which likely saw an even stronger double-digit drop in Q1, due to plummeting travel and transport services around in the world. Trade in services should take longer to recover as transport and travel restrictions remain in place even while domestic lockdowns ease. For this reason, we do not expect global trade of goods and services to exceed 90% of its pre-crisis level by the end of this year.

Figure 1: World merchandise trade and EH Trade Momentum Index

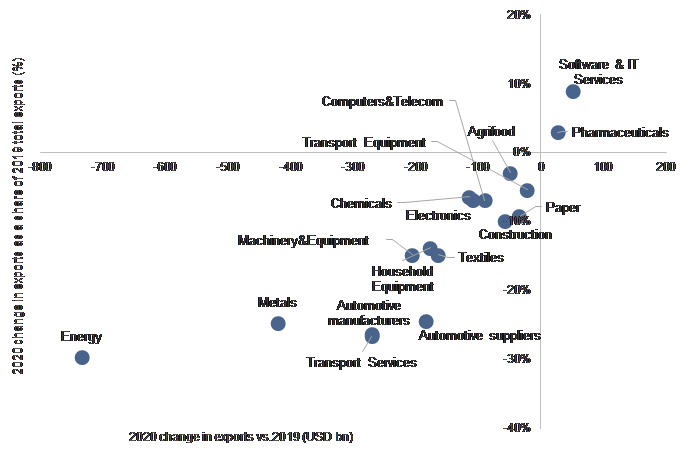

What does this mean for companies? In 2020, we expect the energy sector to be hit the hardest (-USD733bn export losses), followed by metals (-USD420bn) and transport services tied with automotive manufacturers (-USD270bn). While machinery and equipment, textiles and automobile suppliers will lose less in absolute value, the value of their exports will plummet by more than 15%. The only unscathed sectors should be software and IT services (+USD51bn export gain) and pharmaceuticals (+USD27bn). The stock market is also pricing in significant damage to the sectors we have identified: year to date, MSCI Energy lost -37% of its value, the auto sector -18%, transportation -16% and metals and mining -11%, while the aggregate MSCI world index lost -12%. Banking sector equities also lost a staggering -39%.

Figure 2: 2020 Change in exports by sector (USDbn) and share of 2019 total exports (%)

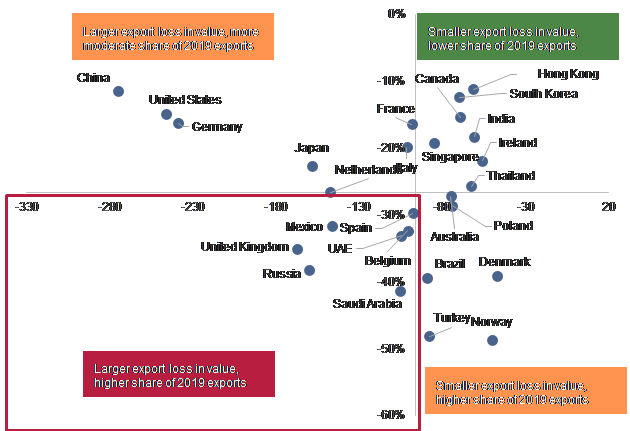

Which country will lose the most? This year barely any country will register export gains compared to 2019. The hardest hit in total value of export losses are, without surprise, the largest exporters: China (-USD275bn), the U.S. (-USD246bn) and Germany (-USD239bn). We rank countries by export losses in absolute value and their share of 2019 total exports. Those who could register high export losses in absolute value and as a share of their total exports are the following: Russia, the UK, Mexico, Spain, the UAE, Belgium and Saudi Arabia.

Figure 3: 2020 Change in exports by country (USDbn) and share of 2019 total exports (%)

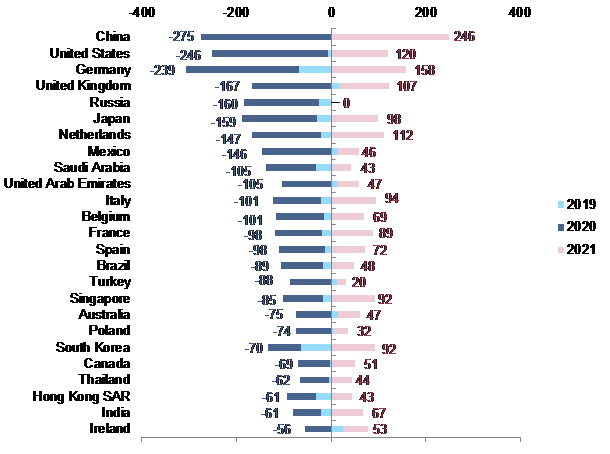

Figure 4: Change in total exports by country (USD bn)

Lastly, short-term protectionist measures on medical goods, the resurgence of economic patriotism rhetoric and reshoring policy stances could disrupt supply chains in the recovery phase and slow the resumption of activity in H2. While China recently slapped Australian barley exports with an 80% tariff, rumors about tariffs on the U.S.’s imports from China are mounting as accusations against Beijing’s role in the Covid-19 crisis intensify. Short-term trade spats could derail confidence, spook markets and halt the investment cycle. Economic historians have demonstrated that the 1930s Great Depression was likely aggravated by the adoption of restrictive trade policies. As recently as in 2019, the U.S.-China trade feud and the manufacturing recession it created subtracted more than USD300bn from global trade.

Medium-term policy shifts also ought to be monitored. The U.S. trade representative hailed the end of offshoring, while the European parliament declared it “supports the reintegration of supply chains inside the EU”. Could a generalized move towards reshoring and decoupling from the Chinese economy make sense?

First, the total reliance on Chinese manufacturing has grown in the past 20 years, rendering reshoring all the more difficult: Not only did Chinese manufacturing as a share of world manufacturing more than double since 2004, but countries have increased their direct and indirect reliance on Chinese inputs (Baldwin and Evenett, 2020). Indeed, China is a supplier of inputs for the U.S.. But it is also a major supplier of auto parts to Germany, Japan, Mexico and Canada. These countries in turn use Chinese inputs when making auto parts and components they sell to U.S.-based automakers, which creates an indirect reliance on China, much larger than the observed reliance.

Second, reshoring does not necessarily mean de-risking: it can also mean putting all your eggs in the same basket, thus creating a risk of pro-cyclicality when the crisis hits. Imagine all sectors become exposed to domestic fluctuations in the economy. If an economy is in lockdown and its factories have to be locked, it cannot really produce everything it needs locally.

Third, growing social discontent could be incompatible with reshoring as it would entail high labor costs passed down to the consumer. While strategic independence is touted by policymakers, raising the price for key durables such as automobiles or everyday electronic items could be unpopular and politically delicate.

Lastly, beyond political arguments, incentives for businesses to reshore are still lacking, and they could cost a lot of public money, possibly passed down to taxpayers. Will companies take it on their margins? Will all governments manage to bypass Ricardo’s comparative advantage and allocation of labor where it’s cheaper? As of today there seems to be a discrepancy between ambitious policy stances and business incentives.

But it’s not only trade that could be disrupted, as more diligent foreign direct investment screening could slow cross-border capital flows. According to the OECD, in most recent years, around 55% to 65% of global Foreign Direct Investment inflows went into countries that apply cross-sectoral review FDI processes – twice the share of global FDI inflows that were potentially subject to security-motivated screening for most of the 1990s. The Covid-19 crisis is likely to accelerate this trend, with the EU and the UK notably potentially tougening their screening rules. UNCTAD predicts a drastic drop in global FDI flows – up to 40% – during 2020-2021, reaching the lowest level in two decades.

:quality(30)/business-review.eu/wp-content/themes/business-review/assets/images/no-picture.png)

:quality(80)/business-review.eu/wp-content/uploads/2024/06/COVER-1-4.jpg)

:quality(80)/business-review.eu/wp-content/uploads/2024/06/br-june-2.jpg)